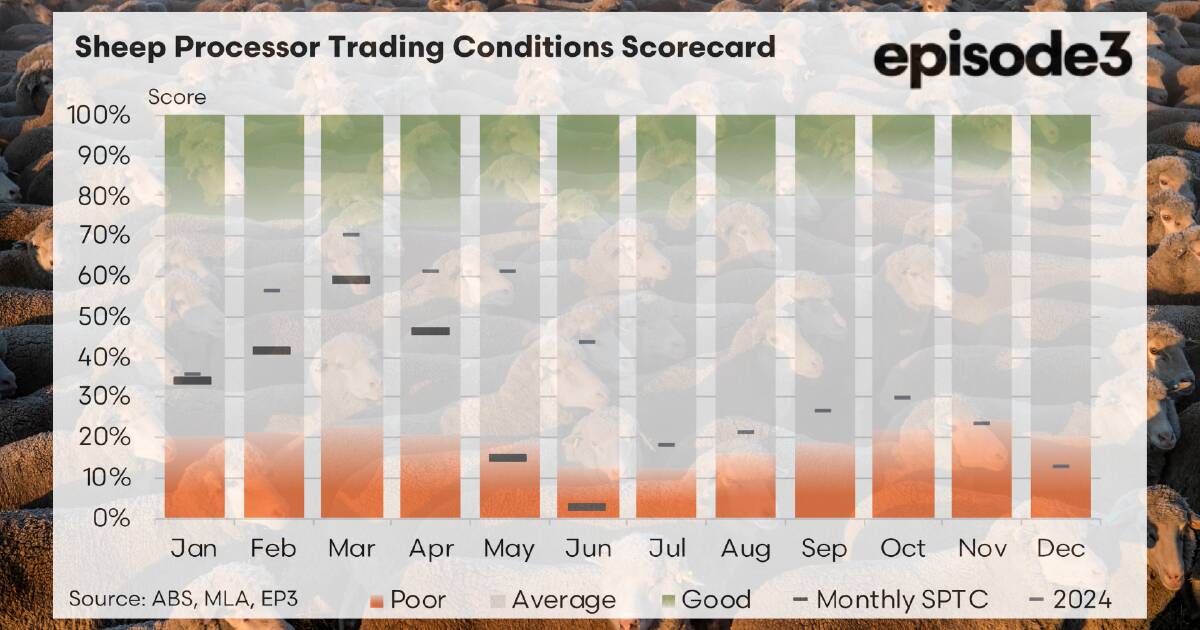

The sheep processing industry is grappling with a significant decline in trading conditions, as evidenced by the SPTC index plummeting to just 2 percent in June. This marks the lowest reading since March 2020 and reflects a downward shift in the annual average score from 39 percent to 33 percent during the month. The ongoing struggle is largely attributed to escalating livestock procurement costs, which are being exacerbated by inconsistent export returns and mixed performance from co-product sales.

Rising Input Costs and Stagnant Export Prices

The sharp increase in livestock prices has been the primary driver of this downturn. In June, lamb values skyrocketed by 16 percent, while mutton prices rose by 14 percent. This surge occurs simultaneously with a lack of corresponding gains in downstream markets, squeezing processors financially. Export performance in June offered little respite, as average export prices for sheepmeat fell by 3 percent compared to May.

Market conditions varied significantly. The United States experienced an 11 percent drop in export values, a notable setback given its importance for high-value cuts. The United Arab Emirates also struggled with a 1 percent decrease in values. Conversely, Malaysia reported a modest 3 percent increase, while China showed resilience with an 8 percent rise in export values. Despite some positive signs, the overall trend remains negative for export prices.

Domestically, retail lamb prices remained almost unchanged, increasing by only 0.4 percent in the June quarter. Although stable consumer pricing may support retail demand, it does little to mitigate the rising procurement costs faced by processors. The domestic market, being relatively small compared to export destinations, leaves processors reliant on international buyers for sustainable profitability.

Mixed Results from Co-Product Revenue Streams

The non-meat revenue streams, which typically bolster processor profitability, also delivered inconsistent results. Tallow prices fell by 15 percent in June, negatively impacting an important co-product revenue source. This decline follows earlier volatility and reflects weakened demand from industrial users, particularly in the biofuel sector. On a brighter note, other co-product receipts, such as offals and skins, improved by 10 percent compared to May, providing some cushioning against the downturn.

Despite these slight improvements, the overall impact on processor margins has been severe. The June results highlight a continued cost-price squeeze that has characterized much of 2025, now more pronounced than at any prior point in the current cycle. The escalating livestock prices reflect heightened competition for stock, particularly as seasonal conditions appear more favorable. While this benefits sellers in the short term, it complicates the situation for processors striving to maintain profitable operations.

Looking at the first half of 2025, the annual average index stands well below the five-year trend. Earlier months, particularly March and April, offered some relief with boosts in co-product and tallow values, but the heavy declines in May and June have overshadowed those gains. Processors now face the dilemma of balancing operational viability against the need to cut production to minimize losses.

The resilience of the Chinese market in June serves as one of the few positive indicators. The 8 percent increase in export values to China demonstrates sustained demand across various product specifications. Malaysia’s modest improvement is also encouraging, particularly given its steady growth in recent years. Nonetheless, the heavy reliance on a few key markets exposes the sector to risks associated with fluctuations in these regions, as evidenced by the significant drop in U.S. returns.

Looking ahead, processors are bracing for a challenging winter. Livestock prices have remained elevated during July and August, and if export values do not rise sufficiently to offset procurement costs, further margin compression is likely. The ongoing softness in tallow markets compounds the challenges facing the industry. While there is potential for co-product values to continue growing, a broader uplift across all revenue streams is essential to alleviate the significant financial strain on processors.

The June data paints a troubling picture of an industry struggling with profitability. The collapse of the SPTC index to 2 percent is not merely reflective of transient market volatility but highlights deeper structural supply pressures within the sheep processing sector.