UPDATE: Australia is set to achieve a historic milestone in beef production, with volumes expected to reach 2.9 million metric tonnes in 2025. This marks an impressive 11 percent increase compared to 2024 levels, according to a newly released report from Rabobank.

The surge in production is primarily driven by increasing cattle slaughter rates and high carcass weights. As a result, beef exports are also on track to hit record levels, soaring 15 percent in the first ten months of 2025 to reach 1.3 million metric tonnes. This robust performance is crucial as it aligns with the rising global demand for beef.

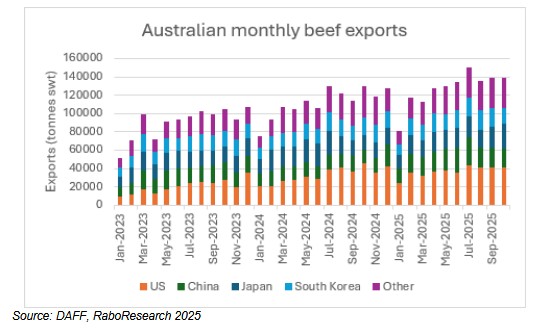

Angus Gidley-Baird, senior animal proteins analyst at Rabobank, highlighted that the United States remains the largest market for Australian beef, comprising 29 percent of total exports. Notably, while grassfed beef accounts for the majority of shipments to the U.S., grainfed beef exports have surged 20 percent this year, reaching 14,000 metric tonnes.

In addition, exports to China have skyrocketed by 44 percent during the same period, with grainfed beef to China increasing by an astounding 58 percent. Gidley-Baird attributes this growth to a decrease in U.S. beef exports to China, allowing Australia to fill the gap.

Current seasonal conditions are pivotal for the Australian cattle market. Gidley-Baird explained that cattle prices are significantly influenced by these conditions and producer sentiment. After a period of drier weather that affected cattle-producing areas through September and October, prices dipped. However, improved rainfall in late October has led to a rebound in prices, a trend expected to persist into 2026.

On a global scale, beef production is experiencing a decline. Key producing regions are forecasted to see a 0.8 percent contraction in output for 2025 compared to last year. New Zealand is projected to face the most significant drop at 4.7 percent, while the United States anticipates a reduction of nearly 500,000 metric tonnes or 4 percent. Canada and the EU27+UK are also expected to experience contractions of 3.9 percent and 3 percent, respectively.

Given these dynamics, Australia’s beef production is positioned for growth, alongside China’s expected 1 percent increase driven by higher culling rates. Meanwhile, Brazil forecasts a modest growth of 0.5 percent for 2025 due to stronger-than-anticipated production earlier in the year.

The Rabobank report also indicates that cattle prices in the northern hemisphere remain elevated, even as they slightly dipped in the U.S. and Canada through September and October. Conversely, southern hemisphere prices are trending upward, driven by demand for beef in northern markets.

The U.S. trade policies continue to shape beef trade dynamics. Argentina’s increased quota into the U.S. will enable more beef at reduced tariff rates, but these production volumes will take time to scale up. Additionally, the recent decision to eliminate a 40 percent tariff on Brazilian beef is anticipated to boost Brazilian exports to the U.S., intensifying competition for Australian beef.

Despite these challenges, strong demand in the U.S. market is expected to keep Australian beef exports robust. The outlook for the beef industry remains promising as producers adapt to changing global conditions and capitalize on emerging opportunities.

As developments unfold, stakeholders in the agricultural sector and consumers alike should stay alert to these shifts impacting production and trade in the global beef market.